GASB 74/75 frequently asked questions

General information

The Governmental Accounting Standards Board (GASB) is an independent, non-profit, non-governmental regulatory body charged with setting authoritative standards of accounting and financial reporting for state and local governments, including school employers. GASB accounting standards are the primary source of Generally Accepted Accounting Principles (GAAP) for state and local governments, including CalSTRS and school employers.

GASB Statement No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, establishes financial reporting standards for state and local governmental other postemployment benefit (OPEB) plans – defined benefit OPEB plans and defined contribution OPEB plans that are administered through trusts or equivalent arrangements.

GASB 74 replaced GASB 43, Financial Reporting for Post-Employment Benefit Plans Other Than Pension Plans, as amended, and GASB 57, OPEB Measurements by Agent Employers and Agent Multiple- Employer Plan. It became effective for financial statements for fiscal years beginning after June 15, 2016. CalSTRS first implemented this standard in our Annual Comprehensive Financial Report for the fiscal year ended June 30, 2018.

GASB 74 is applicable to CalSTRS which administers an OPEB plan called the Medicare Premium Payment (MPP) Program. The standard requires the establishment of a net OPEB liability to be measured as the total OPEB liability, less the amount of the OPEB plan’s fiduciary net position. The statement also requires additional disclosure and supplementary information to be included in the OPEB plan’s financial statements.

GASB 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions, established standards of accounting and financial reporting for defined benefit OPEB and defined contribution OPEB that are provided to the employees of state and local governmental employers through OPEB plans that are administered through trusts or equivalent arrangements.

GASB 75 replaced GASB 45, Accounting and Financial Reporting by Employers for Postemployment Benefits Other Than Pensions. It applies to the GAAP-based financial statements of employers and became effective for the fiscal years beginning after June 15, 2017.

This standard is applicable to the employers who participate in the MPP Program and requires employers to report a liability equal to their proportionate share of the collective OPEB liability for all entities participating in CalSTRS’ cost-sharing plan on the face of the financials. In addition, employers are required to present more extensive note disclosures and required supplementary information about their net OPEB liability.

The Medicare Premium Payment Program is a cost-sharing multiple-employer other postemployment benefit plan established pursuant to Chapter 1032, Statutes of 2000 (SB 1435). CalSTRS administers the MPP Program through the Teachers’ Health Benefits Fund.

The MPP Program pays Medicare Part A premiums and Medicare Parts A and B late enrollment surcharges for eligible members of the Defined Benefit (DB) Program who were retired or began receiving a disability allowance prior to July 1, 2012, and were not eligible for premium free Medicare Part A.

The payments are made directly to the Centers for Medicare and Medicaid Services on a monthly basis.

The CalSTRS MPP Program is available to eligible members of the DB Program who are 65 years or older. These members must be enrolled in Medicare Part A or B, and must be ineligible to receive premium free Medicare A coverage on their own.

Members who retired or were receiving a disability allowance prior to January 1, 2001, are eligible to have CalSTRS pay their Medicare Part A premium and Part B surcharges. Members who retired on or after January 1, 2001, but before July 1, 2012, must meet all of the criteria above and must have retired from an employer who held a Medicare Division.

If the Medicare Division was held before January 1, 2001, the member is eligible. If the Division was held on or after January 1, 2001, and the member was less than 58 years old at the time of the Division, they must have elected to receive Medicare coverage.

Members who were receiving a disability allowance, and were actively employed at the time of the Division, must meet all of the same criteria as above. Members who were receiving a disability allowance, but were not actively employed are also eligible, as long as the Division was completed prior to the time the member reached normal retirement age.

A Medicare Division is an election where a member makes an irrevocable choice whether or not to be covered by Medicare through the payment of Medicare payroll tax. These elections were overseen and conducted by the California Public Employees Retirement System.

DB Program members who were hired prior to April 1, 1986, were not required to pay Medicare payroll tax. All members hired after April 1, 1986, were required to pay the Medicare payroll tax, as such pre-1986 hires had to opt in or out.

Per Education Code § 41010, all Local Educational Agencies are subject to the California School Accounting Manual, as approved by the State Board of Education and furnished by the Superintendent of Public Instruction.

The California School Accounting Manual requires most school employers to prepare their financial statements in accordance with Generally Accepted Accounting Principles. GASB standards, including GASB 75, are the primary source of GAAP for most school employers. Conformity with GAAP allows comparability among school employers. Being out of compliance with GAAP may impact the audit opinion of the school employer’s financial statements.

Any participating employer that is a member of one of the state’s defined benefit plans must implement GASB 75, including local governments, public authorities, and local school systems. Not for profit charter schools that use the full-accrual basis of accounting may need to report these amounts in their financial statements.

GASB 74 and GASB 75 do not establish requirements for funding. The statements aim to separate funding and financial reporting and provide users with information about the effects of OPEB-related transactions and other events on the face of the basic financial statements.

GASB 75 takes an accounting-based approach to assist users in assessing accountability and relationship between government’s inflows of resources and its total cost of providing government services each period.

No. The MPP Program is funded on a pay-as-you go basis from a portion of monthly employer contributions to the DB Program. In accordance with California Education Code Section 25930, contributions that would otherwise be credited to the DB Program each month are instead credited to the MPP Program to fund monthly program and administrative costs. Total redirections to the MPP Program are monitored to ensure that total incurred costs do not exceed the amount initially identified as the cost of the program.

Statutory contribution rates for participating State Teachers’ Retirement Plan employers are determined by the legislature, which has given the Teachers’ Retirement Board limited authority to adjust the supplemental employer contribution rate from July 1, 2021, through June 2046 in order to eliminate the remaining unfunded actuarial obligation related to service credited to members prior to July 1, 2014.

No. The NOL is an accrual accounting measurement calculated in conformity with GASB 74 and GASB 75. The unfunded liability is a funding measure calculated according to Actuarial Standards of Practice.

Net Other Postemployment Benefit Liability

The net OPEB liability of the MPP Program is presented in multiple places within the Financial section of the Annual Comprehensive Financial Report.

- Note 4 - Net OPEB liability of employers

- Schedule V - Schedule of changes in net OPEB liability of employers

- Schedule VI - Schedule of net OPEB liability of employers

Information on the discount rate for the MPP Program may be found in Note 4 of the notes to the basic financial statements within the Financial Section of the Annual Comprehensive Financial Report.

The MPP Program is funded on a pay-as-you-go basis, with contributions generally being made at the same time and in the same amount as benefit payments. As such, the fiduciary net position will not be sufficient to make the projected future benefit payments.

Since the MPP Program is essentially unfunded from a financial reporting perspective, in accordance with GASB 74, the rate used to discount the total OPEB liability represents the yield or index rate for 20-year, tax-exempt general obligation municipal bonds with an average rating of AA/Aa or higher.

No, the NOL is an accrued liability, similar to accrued vacation or other employment benefits that have been earned by employees but are payable sometime in the future. The program is funded on a pay-as-you-go basis with contributions generally being made at the same time and in the same amount as benefit payments and expenses coming due. Additionally, each employer's individual liability represents a proportionate share of the collective OPEB liability as of a given fiscal year end for all entities participating in the MPP Program. Therefore, school employers have no mechanism for directly reducing their liability.

The NOL for individual employers can only be reduced when the collective NOL of the MPP Program decreases.

Proportionate share calculation

Due to the unique approach by which the MPP Program is funded, each employer may have different accounting policies for determining their proportionate share of the NOL, OPEB expense, and deferred inflows and outflows. CalSTRS prepares the schedule of proportionate share of contributions for employers and nonemployer contributing entity (Schedule A) in CalSTRS’ Other Pension Information (OPI) report, to assist employers with meeting the requirements of GASB 68. Employers can also use this report to calculate a proportionate share factor that can be applied to the NOL of the MPP Program for GASB 75 purposes.

Schedule A shows each employer’s contributions (to the nearest dollar) as calculated by CalSTRS along with any additional allocated contributions (note: no additional allocated contributions were applicable to the June 30, 2024, Schedule A). It also shows corresponding contributions for each individual employer as a percentage of total employer contributions (which includes employer contributions made by the State of California as a nonemployer contributing entity to the State Teachers’ Retirement Plan) for the fiscal year. The percentage is displayed to three decimal places.

As the State of California does not make contributions to the MPP Program, those State of California contributions shown in Schedule A should be excluded from total employer contributions when considering the proportionate share factor for the net OPEB liability. As such, employers will need to recalculate their proportionate share factor using information presented in Schedule A. To do this, employers would divide their total CalSTRS calculated and allocated contributions by Total CalSTRS-calculated employer contributions at the bottom of Schedule A.

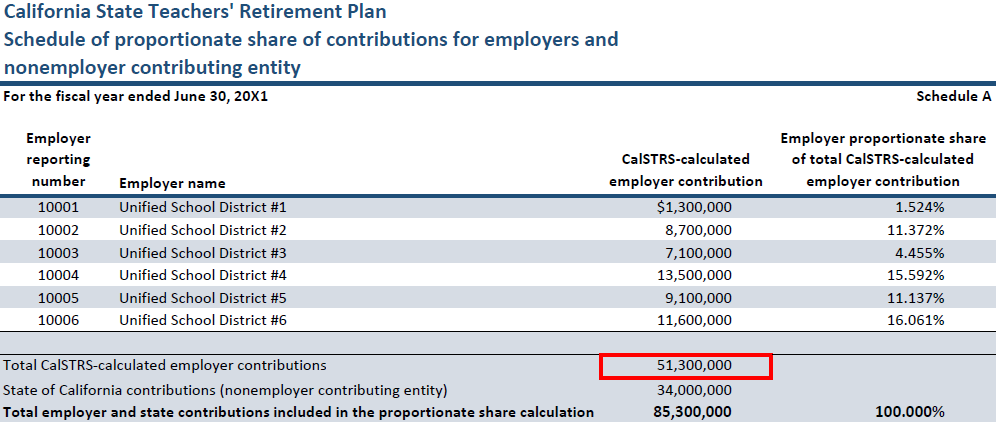

The following is a screenshot of a fictional Schedule A for the fiscal year ended June 30, 20X1 to be used for example purposes:

Based on the data above, Unified School District #1 would use this Schedule A to recalculate its proportionate share factor for the MPP Program by excluding the nonemployer contributing entity (State of California) as follows:

[A] | Unified School District #1 – Total calculated and allocated contributions (Schedule A) | $1,300,000 |

|---|---|---|

[B] | Total CalSTRS-calculated employer contributions (Schedule A) | $51,300,000 |

[A] / [B] | Recalculated proportionate share factor for GASB 75 purposes excluding nonemployer contributing entity | 2.534% |

The following is an example of calculating Unified School District #1's proportionate share of the net OPEB liability, which can be found within Note 4 (Net OPEB liability of employers) of the Annual Comprehensive Financial Report). This calculation uses a fictional net OPEB liability of employers as of June 30, 20X1, along with the recalculated proportionate share factor (taken from the previous question) for example purposes.

[A] | Net OPEB liability of employers (Note 4) | $400,000,000 |

|---|---|---|

[B] | Recalculated proportionate share % based on total employer contributions (excluding State of California contributions) | 2.534% |

[A] * [B] | Unified School District #1’s share of the net OPEB liability | $10,136,000 |

Employers may use this process each year to calculate their current proportionate share factor, and NOL.

No, school employers are not required by the new accounting standards to use the proportionate share calculated by CalSTRS. Each employer’s method of determining their proportionate share of the net OPEB liability, deferred inflows and outflows of resources, and OPEB expense of the MPP Program is an accounting policy decision that each employer should consult on with their auditors.

CalSTRS calculates current year contributions due based on current year creditable earnings for active members as reported by employers. Since cash remittances of contributions due are received from employers prior to reports of creditable earnings by member, CalSTRS accrues employer contributions due monthly based on estimates. In addition, CalSTRS recognizes contributions and adjustments to contributions reported in the current year for service performed in a prior year as they are reported by employers.

The specific types of contributions included are:

- Monthly contributions, including accruals, to the Defined Benefit Program for the CalSTRS 2% at 60 under Education Code §§ 22950 and 22951.

- Monthly contributions, including accruals, to the Defined Benefit Program for the CalSTRS 2% at 62 formula under Government Code § 7522.30.

- Excess service contributions, including accruals, to the Defined Benefit Supplement Program under Education Code § 22905(b)(1).

- Employer contributions to the Cash Balance Benefit Program under Education Code §§ 26503 and 26503.5.

- Employer contributions to the Defined Benefit Supplement Program for limited-term compensation increases under Education Code § 22905(b)(3).

- Employer contributions for members who participate in the reduced workload program under Education Code § 22713(e).

- Employer contributions for members which serve as an elected officer in an employee organization under Education Code § 22711(a)(3).

- Employer contributions redirected to the Medicare Premium Payment Program under Education Code § 22950(c).

- Employer contributions redirected to the Teachers’ Replacement Benefits Program under Education Code § 24260(d).

CalSTRS excluded the following contributions from Schedule A because they are separately financed obligations paid in installments, or do not reflect the employers’ long-term contribution effort:

- Employer contributions to the Supplemental Benefit Maintenance Account and the Defined Benefit Program for retirement incentives (golden handshake) under Education Code §§ 22714 and 22715.

- Employer contributions for the purchase of one-year final compensation under Education Code § 22135(f).

- Employer contributions for service credit awarded for excess unused sick leave under Education Code § 22718.

- Employer contributions for additional service credit under Education Code § 22801(d).

- Employer contributions for military service credit under Education Code § 22852.

To help employers understand the amount presented for their school district in Schedule A - Schedule of proportionate share of contributions for employers and nonemployer contributing entity, CalSTRS has provided a reconciliation of employer contributions report through the Contributions Account Portal.

To get to the report, school employers must log into the Secure Employer Website and then follow this path:

Contribution Account Portal ➤ Financial Reporting ➤ Reconciliation of Employer Contributions

There is a job aid on the Help page on the Contributions Account Portal that explains in detail how to run the report. A link to the job aid is also posted on CalSTRS.com.

The reconciliation of employer contributions report reconciles contributions presented in Schedule A to contribution reports submitted by employers. However, it does not include information on contributions by the state on behalf of employers.

Deferred inflows/outflows

A traditional balance sheet consists of assets and liabilities; however, GASB felt these categories were insufficient to describe certain transactions. As such, GASB created two new categories known as deferred inflows of resources and deferred outflows of resources.

GASB first introduced the idea of deferred inflows and outflows of resources in Concepts Statement No. 4, which defines deferred outflows of resources as a consumption of net assets that is applicable to a future reporting period. Concepts Statement No. 4 defines deferred inflows of resources as an acquisition of net assets that is applicable to a future reporting period. Deferred outflows of resources balances have a positive effect on net position, similar to assets, and deferred inflows of resources balances have a negative effect on net position, similar to liabilities.

Typically, when assets and liabilities are recorded, they have a corresponding revenue or expense that is recognized in the current period. Conversely, when deferred items are recorded, the expense or revenue is recognized in future periods (like a prepaid expense or deferred revenue).

GASB 75 classifies the following items as deferred inflows and outflows:

- Differences between expected and actual experience. (1)

- Changes in assumptions.

- Net difference between projected and actual earnings on plan investments.

- Changes in proportionate share.

- Contributions subsequent to the measurement date.

- Difference between an employer’s proportionate share and actual contributions.

(1) Also referred to as actuarial gains and losses.

The amortization period for the difference between projected and actual earnings on plan investments is five years. The amortization period for all other deferred items is the average remaining service life of plan members.

Except for the difference between projected and actual earnings on plan investments, deferred inflows and outflows must be separately recognized and amortized in the financial statements. They cannot be netted together.

For example, if there is a deferred outflow of resources of $200 and a deferred inflow of resources of $500 related to changes in assumptions, they cannot be combined and shown on the balance sheet as a $300 net deferred inflow of resources for changes in assumptions. However, deferred inflows and outflows for the difference between projected and actual earnings on plan investments is an exception and can be netted together.

As the MPP Program is a retiree only OPEB plan with no active members, the average remaining service life is one year.

CalSTRS will maintain schedules for deferred inflows of resources and deferred outflows of resources specific to the OPEB plan at the collective level. However, employers will need to maintain schedules for deferrals arising from changes in the employer’s proportionate share and contributions subsequent to the measurement date.

The reasoning behind this approach is that CalSTRS is not calculating deferrals specific to individual school employers.

Employers who participate in the MPP Program are required by GASB 75 to disclose their district’s proportionate share of the MPP Program’s deferred inflows and outflows of resources and OPEB expense. Deferred outflows and inflows of resources for the MPP Program can be found within the GASB 74/75 Financial Reporting actuarial valuation reports.

Reporting

Yes, changes resulting from GASB 75 requirements apply to the government-wide financial statements, enterprise and agency funds financial statements which are prepared on full accrual basis of accounting.

The measurement date is the date the net OPEB liability is measured for purposes of a school employer’s financial reporting and must be consistently applied from period to period. GASB 75 requires the total OPEB liability be determined by (a) an actuarial valuation as of the measurement date or (b) the use of update procedures to roll forward to the measurement date amounts from an actuarial valuation as of a date no more than 30 months and 1 day earlier than the employer’s most recent fiscal year end.

As the collective NOL is reported by CalSTRS, the measurement date must fall on June 30, which is CalSTRS fiscal year end.(2) However, school employers can choose to use June 30 of the current fiscal year or June 30 of the prior fiscal year as the measurement date.

For example, for their financial statements for the fiscal year ending June 30, 2024, school employers can use June 30, 2023, or June 30, 2024, for their measurement date.

When selecting the measurement date, school employers should consider when CalSTRS financial statements will be available in relation to when the employer plans to complete their own financial statements.

Employers who choose to use a measurement date of June 30 from the current fiscal year should consider that CalSTRS’ June 30 financial statements are generally not available until November of the same calendar year following their presentation to the Teacher’s Retirement Board. For example, if an employer is reporting for June 30, 2024, and uses a measurement date of June 30, 2024, they would need to use information from CalSTRS’ June 30, 2024, financial statements, which would not be available until November 2024.

(2) June 30 is also the fiscal year end for school employers, per the Department of Education’s California School Accounting Manual.

CalSTRS' current fiscal year financial statements are contained within the Annual Comprehensive Financial Report, which is available on CalSTRS.com.

CalSTRS’ audited June 30 financial statements are posted to CalSTRS.com following their presentation to the Teachers’ Retirement Board in November. The financial statements are contained within the Annual Comprehensive Financial Report which is made available online in late December once it’s completed.

GASB 75, paragraphs 89-98, describe the required note disclosures and the required supplementary information for cost-sharing employers. Unfortunately, CalSTRS cannot assist employers in preparing this information as it falls outside the scope of CalSTRS fiduciary duty to our members.

The MPP Program is a cost-sharing multiple-employer other postemployment benefit plan established pursuant to Chapter 1032, Statutes 2000 (SB 1435).

As a cost-sharing multiple-employer OPEB plan, OPEB obligations to the employees of more than one employer are pooled and OPEB plan assets can be used to pay the benefits of the employees of any employer that provides OPEB through the OPEB plan. In accordance with GASB 75, cost-sharing employers are required to recognize a liability for their proportionate share of the net OPEB liability.

Per Education Code § 41010, all Local Educational Agencies are subject to the California School Accounting Manual, as approved by the State Board of Education and furnished by the Superintendent of Public Instruction.

The California School Accounting Manual requires most school employers to prepare their financial statements in accordance with Generally Accepted Accounting Principles. GASB standards, including GASB 75, are the primary source of GAAP for most school employers.

Being out of compliance with GAAP may impact the audit opinion of the school employer’s financial statements. Employers are encouraged to consult with their independent auditors about these GASB standards and the policies needed to implement the changes outlined above.

Additional information

CalSTRS identifies links to additional information that may be helpful to employers on CalSTRS.com.

CalSTRS cannot give specific accounting advice or guidance to employers, but for questions about GASB 74 and GASB 75, contact CalSTRS’ Financial Reporting team at FinancialReporting@CalSTRS.com.